At A Glance

The long-awaited HHS Provider Relief Funding post reporting instructions were released on September 19, 2020. These new instructions mark a significant shift from the FAQs originally included as part of the funding distributions. Specifically, rather than starting with lost revenue calculations in determining the use of the funds, the instructions indicate that coronavirus-related expenses be considered first. Additionally, the expenses should be considered only to the extent they were not reimbursed by other sources. This may have a substantial impact on many providers as they look to justify their use of the funds received. Likely, the calculations indicated by the instructions will be more conservative in determining the use of funds than the calculations anticipated by the original FAQs. The following is an overview of the new instructions.

Reporting Requirements

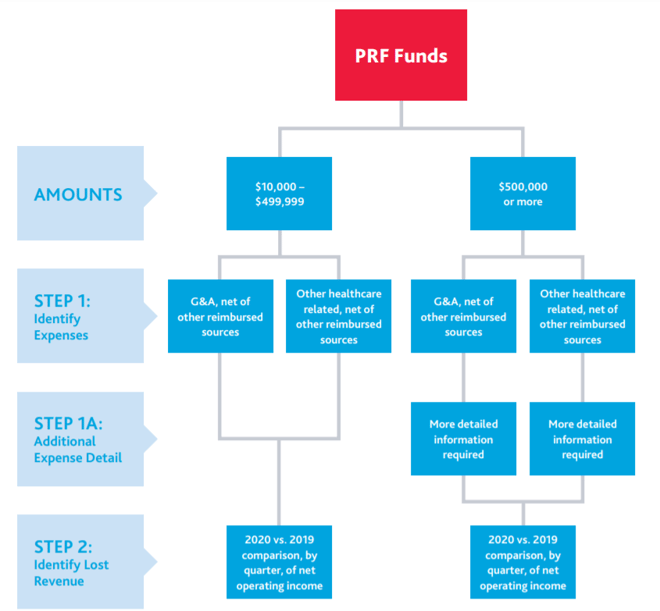

The instructions are meant to give recipients of the Provider Relief Fund (PRF) exceeding $10,000 the requirements for reporting on how their organizations utilized these funds in accordance with the terms and conditions of the various distributions.

The notice outlines data elements for 2019 and 2020 that must be reported as part of this process. The Health Resources and Services Administration (HRSA) will offer webinars, along with FAQs to aid in the reporting. The reporting system will now be available in early 2021 instead of October 1, 2021. The Centers for Medicare & Medicaid Services (CMS) has not yet stated that the reporting deadline for 2020 expenditures has been delayed. As of now, this is still 45 days after the end of 2020, which would be February 15, 2021. Organizations with funds not yet utilized after December 31, 2020, will submit a second and final report by July 31, 2021. This report will focus on the use of the funds from January 1, 2021–June 30, 2021.

Data Elements

Data elements for the reporting are as follows and summarized. For more information, visit HHS Provider Relief Funding post reporting instructions.

Demographic Information

- Reporting Entity: Tax Identification Number of the entity that received the PRF payment.

- Tax Identification Number (TIN): Reporting Entity’s primary TIN associated with the provider who received and accepted the PRF payment during attestation.

- National Provider Identifier (NPI): Unique 10-digit numeric identifier.

- Fiscal Year End Date: Month in which the recipient reports its fiscal year-end financial results.

- Federal Tax Classification: Designated business type.

Facility, Staffing and Patient Care Metrics

- Personnel Metrics: Total personnel by labor category (full-time, part-time, contract, other: recipient must define), total re-hires, total new hires, total personnel separations by labor category.

- Patient Metrics: Total number of patient visits (in-person or telehealth), total number of patients admitted, total number of resident patients.

- Facility Metrics: Total available staffed beds for medical/surgical, critical care, and other beds.

Use Of Funds

As previously mentioned, clarifying the determination of the use of funds included in the instructions appears somewhat different than what many interpreted from the FAQs.

The following is an overview of the process per the instructions:

Expenses

Calendar year 2020 expenses attributable to coronavirus may be incurred both in treating confirmed or suspected cases of coronavirus, preparing for possible or actual coronavirus cases, and maintaining healthcare delivery capacity. These expenses must be actual expenses incurred over and above what has been reimbursed by other sources.

Entities receiving between $10,000 and $499,999 are required to report healthcare-related expenses into the following categories:

- General and Administrative Expenses (G&A)

- Other healthcare related expenses

Recipients of funding $500,000 or more will report expenses attributable to coronavirus in the same two categories of G&A expenses and other healthcare-related expenses. These facilities will need to report in more detail than the other facilities.

Per the reporting guidelines, G&A expenses are outlined as follows:

- Mortgage/Rent: Monthly payments related to mortgage or rent for a facility.

- Insurance: Premiums paid for property, malpractice, business insurance, or other insurance relevant to operations.

- Personnel: Workforce-related actual expenses paid to prevent, prepare for, or respond to the coronavirus during the reporting period, such as workforce training, staffing, temporary employee or contractor payroll, overhead employees, or security personnel.

- Fringe Benefits: Extra benefits supplementing an employee’s salary, which may include hazard pay, travel reimbursement, employee health insurance, etc.

- Lease Payments: New equipment or software lease.

- Utilities/Operations: Lighting, cooling/ventilation, cleaning, or additional third-party vendor services not included in “Personnel”.

- Other General and Administrative Expenses: Costs not captured above that are generally considered part of overhead structure.

Healthcare-related expenses per the reporting guidelines:

- Supplies: Expenses paid for the purchase of supplies used to prevent, prepare for, or respond to the coronavirus during the reporting period. Such items could include personal protective equipment (PPE), hand sanitizer, or supplies for patient screening.

- Equipment: Expenses paid for purchase of equipment used to prevent, prepare for, or respond to the coronavirus during the reporting period, such as ventilators, updates to HVAC systems, etc.

- Information Technology (IT): Expenses paid for IT or interoperability systems to expand or preserve care delivery during the reporting period, such as electronic health record licensing fees, telehealth infrastructure, increased bandwidth, and teleworking to support remote workforce.

- Facilities: Expenses paid for facility-related costs used to prevent, prepare for, or respond to the coronavirus during the reporting period, such as lease or purchase of permanent or temporary structures, or to modify facilities to accommodate patient treatment practices revised due to coronavirus.

- Other Healthcare Related Expenses: Any other actual expenses, not previously captured above, that were paid to prevent, prepare for, or respond to the coronavirus.

|

G&A Expense Types |

Healthcare Related Expense Types |

|

|

Lost Revenue

Lost Revenue as laid out in the reporting guidelines is different than what had been outlined in the FAQs. The guidelines now state lost revenue attributable to coronavirus is represented as a negative change in year-over-year net operating income from patient care related sources. When revenue is determined, cost and expenses will be calculated through a comparison of healthcare expenses for calendar years 2019 to 2020 to arrive at net operating income. Revenues and expenses in this section include all lost patient care revenue and patient care cost/expense impacts. Calendar year actual revenue will be entered by quarter for both 2019 and 2020. Revenue/net charges from patient care (prior to netting with expenses) for the calendar years 2019 and 2020 is to be reported based on the following:

|

Patient Care Payer Mix (2019 and 2020) |

Other Assistance Received (2020) |

|

|

Single Audit Requirement

Entities expending $750,000 or more in federal financial assistance in 2020, which includes PRF payments, are subject to the Single Audit requirements per regulation 45 CFR 75.501. Recipients do need to indicate if they are subject to Single Audit requirements in 2020. If the answer to that question is yes, recipients should indicate whether their auditors selected PRF payments to be within the scope of the Single Audit, if known.

Takeaways

Key takeaways for healthcare organizations from the new instructions include the following:

Use of Funds

The change in priority from assessing the use of funds using lost revenue as the first step to now using expenses as the first step may have a significant negative impact on many organizations. Most organizations were relying on the use of lost revenue to justify a majority of the funds received, with coronavirus expenses comprising the balance. Any coronavirus expenses that exceeded the amount of funds received could be used to to apply for FEMA funding, as appropriate. WIth the change in priority, all coronavirus expenses may be utilized for the PRF funds (thus leaving none to apply for FEMA reimbursement) and the new lost revenue calculation (discussed below) may not be sufficient to justify all of the PRF funds received. As a result, some organizations may have significant unused funds that they are required to repay. Organizations should immediately reevaluate their use of funds calculations and determine if they may potentially have significant paybacks in the future, and if so, identify cash flow strategies to provide for those paybacks. Management should also monitor advocacy efforts that are sure to develop as trade organizations (HFMA, AHA, MGMA, AHCA, and others) begin to evaluate the impacts on providers and consider asking for modifications that are not as restrictive for providers.

Lost Revenue

With the significant change in how lost revenue is calculated, healthcare organizations need to pivot their focus, looking at this from a year-over-year loss in net operating income. Based on this guidance, the concept of lost revenue would only come into play if COVID-related healthcare expenses were less than the amount received from the HHS PRF. This approach provides a more limited method than original guidance. It also limits the amount of lost revenue that can be applied to the funding. Management must evaluate the new definition of lost revenue and how it impacts the initial assessment of its use in determining the use of funds.

Reporting

Reporting will begin in January 2021 and the deadline for reporting the funds utilized in FY 2020 will be before February 15, 2021. Subsequent reporting for the period from January 1, 2021 to June 30, 2021 will be due July 31, 2021. Organizations should ensure that their record-keeping is sufficient to comply with the detailed requirements included in the instructions. Additionally, revenue recognition should be assessed to determine the impact on income statement (revenue) vs. balance sheet (deferred revenue) given the change in the determination of the use of funds.