Written by Michael B. Carr, CPA, CTRC

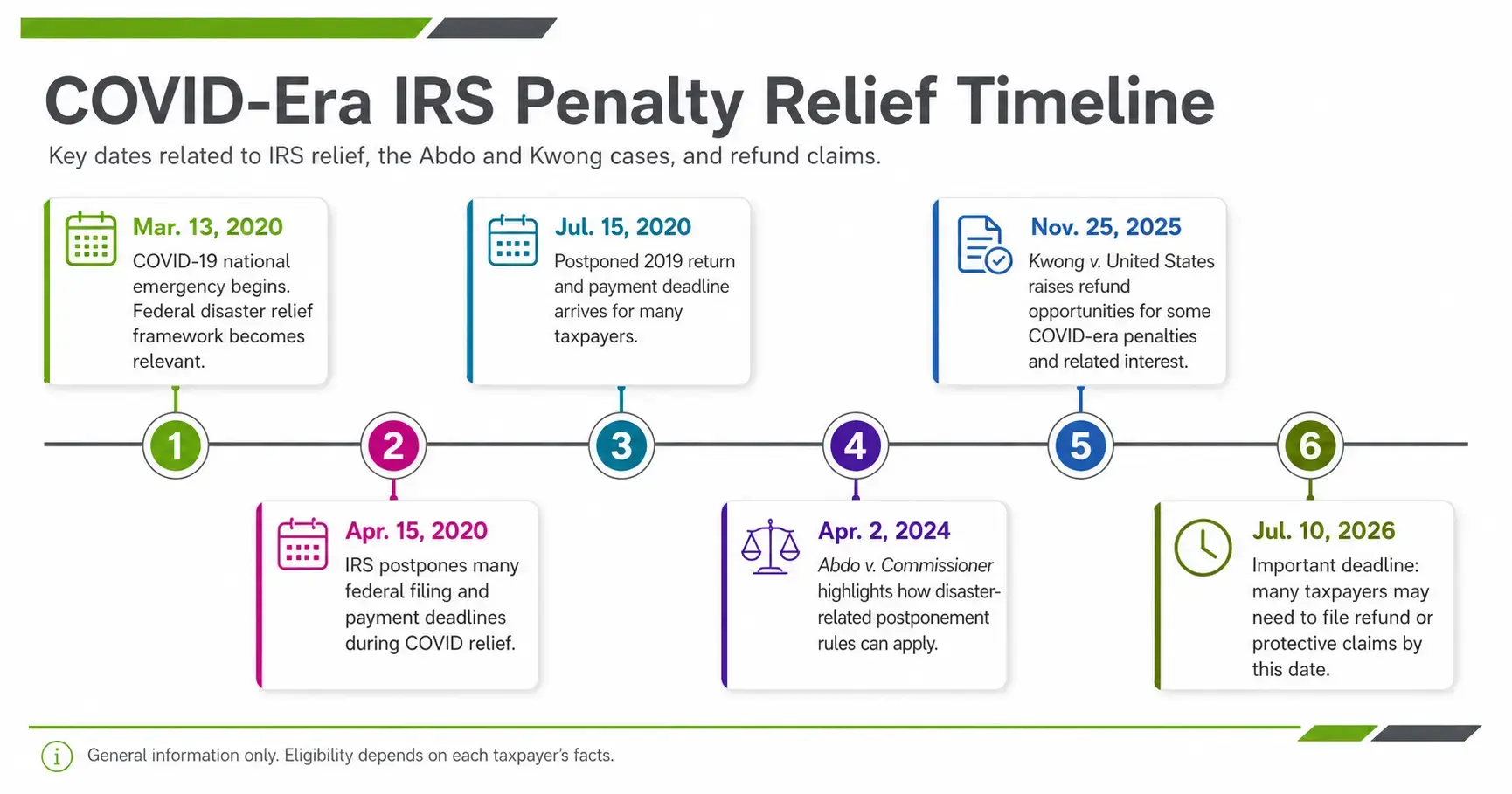

Recent court decisions are creating a meaningful opportunity for taxpayers to seek refunds of certain IRS penalties and the related interest assessed during the COVID-19 period. Notably, this opportunity is not based on traditional “reasonable cause” arguments. Instead, it stems from how the IRS applied (or failed to fully apply) its own COVID-era relief rules.

What Changed?

Two recent cases - Kwong v. Commissioner and Abdo v. Commissioner - focus on the IRS’s implementation of pandemic-related relief under federal disaster provisions.

During COVID-19, the IRS issued guidance postponing certain filing and payment deadlines. Under these rules, when deadlines are properly postponed:

-

Penalties should not apply during the relief period, and

-

Interest tied to those postponed obligations may also need to be adjusted.

These cases challenge the IRS's application of those rules and suggest that, in some situations, penalties and interest were assessed when they should not have been.

Why This Matters

If the IRS postponed the deadline, penalties and related interest may not have been allowable in the first place.

What Relief May Be Available?

If you were assessed IRS penalties during the COVID-19 period, you may be eligible to:

-

Have penalties removed.

-

Receive a refund of penalties already paid.

-

Receive a refund of interest already paid associated with those penalties.

In many cases, interest is reduced automatically when penalties are corrected.

Who May Qualify?

This opportunity may apply to individuals and businesses that had penalties and interest related to filing or payment obligations affected by the COVID-era IRS relief.

Examples include:

Returns or payments originally due during the pandemic relief window, which had:

-

Penalties assessed despite extended or postponed deadlines.

-

Interest charged in connection with those penalties.

Eligibility depends on how the IRS applied the relief rules to your specific situation.

Important Deadline

There are time limits for requesting protective relief from penalties and interest. For many taxpayers, the deadline to file a claim is July 10, 2026.

If a claim is not filed by the applicable deadline, the opportunity may be lost.

How To Request Relief

Relief is not automatic. Taxpayers must submit a formal request to the IRS explaining why penalties and interest should be removed based on the proper application of COVID-era relief rules.

How We Are Helping Clients

Our firm is actively assisting clients by:

-

Reviewing accounts for penalties assessed during the relief period.

-

Identifying where IRS relief provisions may not have been fully applied.

-

Preparing and submitting claims to request refunds of penalties and interest.

Given the volume of impacted taxpayers and the approaching deadline, we are using a structured process to ensure claims are completed efficiently and accurately.

Final Thoughts

Although relief is not guaranteed, these developments represent a significant but time-sensitive opportunity. The key issue is not whether a taxpayer had reasonable cause, but whether the IRS correctly applied its own pandemic relief provisions.

If you believe you may have been affected or would like us to review your situation, we encourage you to reach out to your Trout CPA Contact Manager or complete our Contact Us form.